Beginner's Guide to Mutual Fund Investing in India

Beginner's Guide to Mutual Fund Investing in India

First draft was released on 31st March 2024.

Last updated on 25th June 2024.

You must have heard “Mutual Fund Sahi hai” but how to choose that one good mutual fund (or a basket of funds)? Let’s find out today but let’s first learn about some basic terminology. I will keep using these terms again and again in the guide, so let’s understand them first.

Benchmark

Every mutual fund has a “benchmark” against which it compares its performance. Whenever you read in the news “80% of mutual funds haven’t performed better than their benchmark”, this implies that the mutual fund manager did worse than the index against which they are comparing their performance and that “benchmark” is this index. For example, the Parag Parekh Flexi Cap fund’s benchmark is Nifty 500 TRI, which means that PPFAS management compares its performance with Nifty 500 TRI.

Volatility

Volatility means how much and how frequently is a mutual fund going up and down compared to its average. For mutual funds, volatility is typically measured using variance or standard deviation. High-volatility investments experience significant deviations from the mean, while low-fluctuation investments have minimal deviations within a specific timeframe.

Equities (stocks, equity mutual funds, etc) depend on the broader market and have higher volatility, whereas fixed-income instruments (like debt mutual funds) have less volatility because they involve fixed cash flows. You must have listened to this at bullet-fast speed after every mutual fund ad

“Mutual Funds are subject to market risk, please read the offer documents carefully before investing” which means that mutual funds go up and down as the market moves, so people should be aware of that before investing. Therefore, even if two mutual funds give similar returns, their volatility can affect investor behaviour, leading to panic buying/selling and lesser returns eventually.

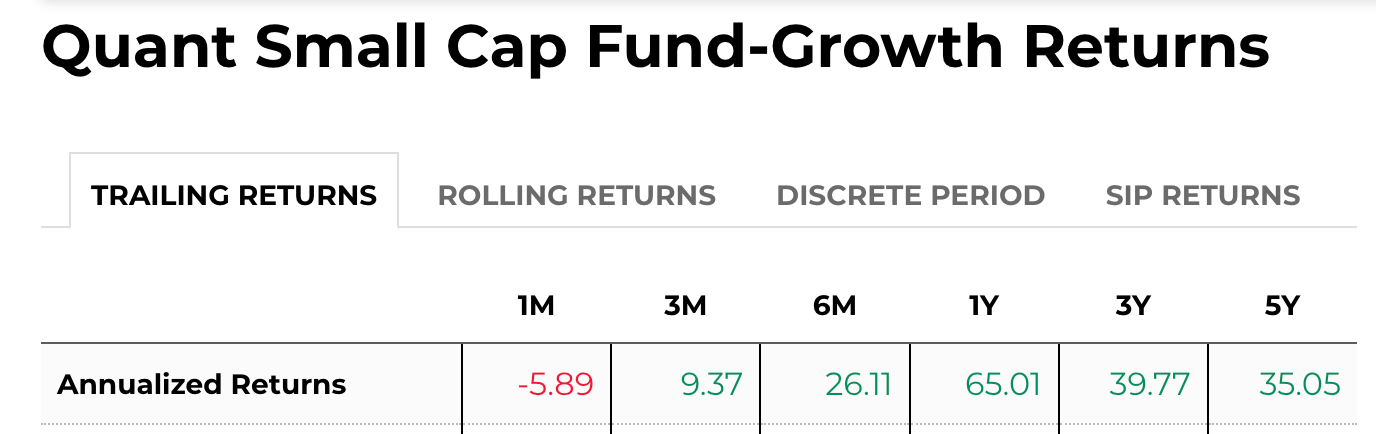

Trailing Returns

99.99% of the people look at the past 1- and 3-year returns and choose the one with the highest. These returns are called “Trailing returns”, meaning how much the fund made during a “point in time” in those number of years. Let’s see an example:

The number 26.11 here means the fund gave 26.11% returns in the past 6 months.

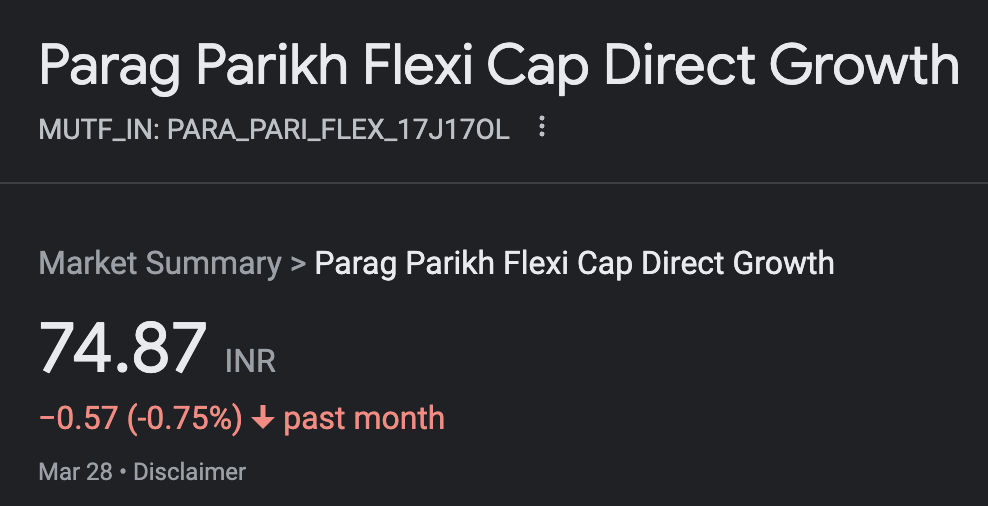

Net Asset Value

Net Asset Value (NAV) is a fundamental metric used to assess the value of a mutual fund. It represents the per-unit value of the fund’s assets after deducting any liabilities. Essentially, NAV indicates the price at which investors buy or redeem mutual fund units.

In this picture, the number 74.87 is called the NAV of this mutual fund, or the price of one mutual fund unit. So if you invest ₹10,000 in this mutual fund, you will get 10,000/74.87 = 133.54 units of this mutual fund. It is like having shares of that mutual fund but you do not need a Demat account for this. Unlike stock prices that fluctuate throughout the day, mutual fund pricing is based on the end-of-day methodology, considering the activity of the securities within the fund’s portfolio.

Expense Ratio

An expense ratio is the cost of owning a mutual fund. Think of it as the management fee you pay to the fund company for holding the fund. It’s expressed as a percentage of your investment. For instance, if you have ₹5,000 invested in a mutual fund with an expense ratio of 0.4%, you’ll pay the fund ₹20 annually. The expense ratio is calculated by dividing a fund’s operating expenses by its net assets. Lower expense ratios are generally better for most investors but more on this in the guide below.

Choosing Index Funds

What are index funds? Most of you might already know but let me reiterate - Index Funds are a class of mutual funds that track a particular index, for example, Nifty 50, Sensex 30, Nifty Next 50, Nifty 200 Momentum 30, etc. But what is meant by tracking? Let’s take the example of Nifty 50.

Nifty 50, as the name suggests, has 50 stocks. If you google “Nifty 50 stocks proportion”, you will see this:

These are just the top 10 stocks but constitute ~56% of the index. Similarly, a mutual fund that tracks the Nifty 50 index also invests in the same 50 stocks in the same proportion which means if the index goes up by 2%, the NAV of this index fund will also go up by almost 2 per cent.

Why did I say “almost”? This is because there is a tracking error, which is the difference between the index return and the mutual fund return. Let’s say that the index goes up by 2.3% and the mutual fund only goes up by 2.25% then the tracking error is 0.05%. But if a mutual fund emulates an index, how is there room for error?

This is because a team of human beings manages a mutual fund and it makes mistakes. The higher the tracking error, the higher the chances you won’t be able to make a return equal to the index. So the first thing you should note while investing in an index fund is its tracking error.

Now, since there isn’t much work to do in the case of an index fund, the Expense Ratio is lower than other mutual funds. So the second thing to consider before investing in an index fund is the Expense Ratio, the lower the better.

A good index fund has a combination of low tracking error and the lowest expense ratio.

Choosing other equity mutual funds

This part will cover different parameters you should consider before investing in equity mutual funds except for the index fund. These funds are also known as “active funds” because the fund manager takes an active part, unlike index funds where there isn’t much work.

Alpha

It is the measure of how much better a mutual fund performs as compared to its benchmark. For instance, if the NIFTY 50 index delivered 10% in the past year and the fund benchmarked against the NIFTY 50 delivered 12%, then the Alpha is +2%. And if the fund underperformed and achieved only 8.5%, then the Alpha is -1.5%. So if you see that a fund has a negative alpha, that implies it’s better to invest in the benchmark fund than in that particular mutual fund.

Beta

This is a measure of how volatile is the mutual fund as compared to its benchmark. So, Beta merely explains the relative riskiness of a mutual fund and does not give the inherent risk of the fund itself. Let’s say the benchmark of a mutual fund goes up by 1% and the beta of the mutual fund is 1.3, then the mutual fund will go up by 1.3%. For low-risk-taking investors, a lower beta is preferable. Beta lower than 1 means the mutual fund’s volatility is less than the benchmark.

The best combination of alpha and beta (if you can find one) would be a mutual fund that has a positive alpha and beta less than 1.

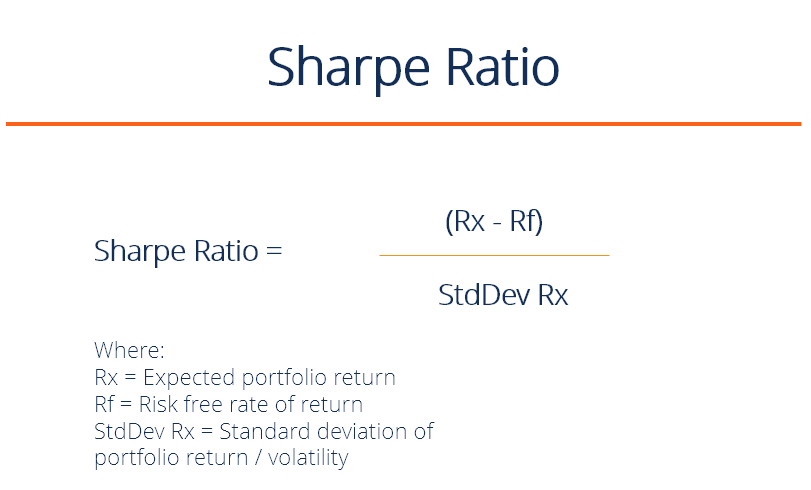

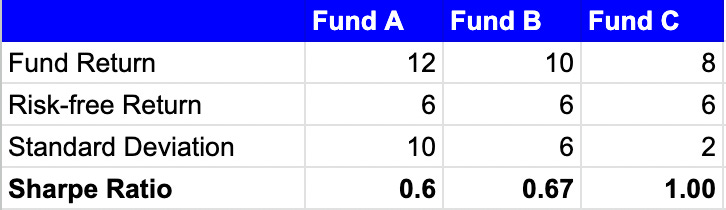

Sharpe Ratio

The Sharpe Ratio measures risk-adjusted performance. It is calculated by subtracting the risk-free rate of return from the fund’s returns and dividing the result by the standard deviation.

Standard deviation is a measure of volatility, the higher the standard deviation, the higher the volatility.

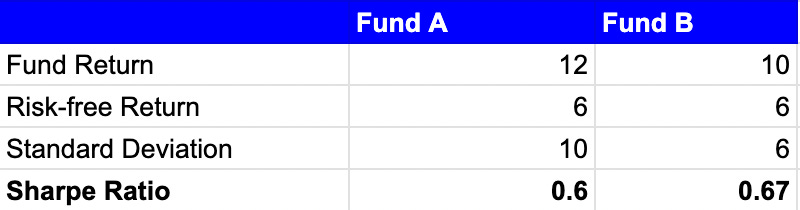

Most finance influencers will say, “The higher the Sharpe Ratio, the better”, but they are wrong and let’s see why.

Fund A generates a return of 12%, while fund B delivers a 10% return.

Although Fund A gave more returns, Fund B gave better “risk-adjusted” returns because its Sharpe Ratio is higher. But we shouldn’t look at this in isolation as it can lead to misleading outcomes, see this example:

Will you be happy with an 8% return? It’s better to invest in an FD than in a mutual fund.

So, while the Sharpe Ratio is a valuable risk measurement tool and you should use it, it is advisable not to use it in isolation when comparing different Mutual Funds.

Capture Ratios

I read about 37 articles before writing this guide but none explained the Capture Ratios, so here it is. Capture Ratios are of two types:

Upside Capture Ratio

The Upside Capture Ratio evaluates a strategy’s performance in up-markets. It measures a manager’s performance relative to its benchmark during rising market conditions. The ratio is calculated by dividing the average strategy returns by the average returns of the benchmark, but only including periods where the benchmark returns were positive.

Downside Capture Ratio

The Down-Market Capture Ratio assesses a strategy’s performance in down markets and measures how well a manager performed relative to the index while the market is falling. It is calculated by dividing the average strategy returns by the average returns of the benchmark, but only including periods where the benchmark returns were negative.

Capture ratios help assess whether a strategy performs according to its investment objective. If the goal of the strategy is to outperform its benchmark, Capture ratios will help demonstrate how the strategy outperformed – whether on the up-side, down-side or overall.

This picture shows these ratios for Parag Parekh Flexi Cap Fund for the past 3 years:

The best combination is to have a mutual fund with a UCR of above 100 and DCR of below 100, even better if these numbers are higher than the cateogry average as well.

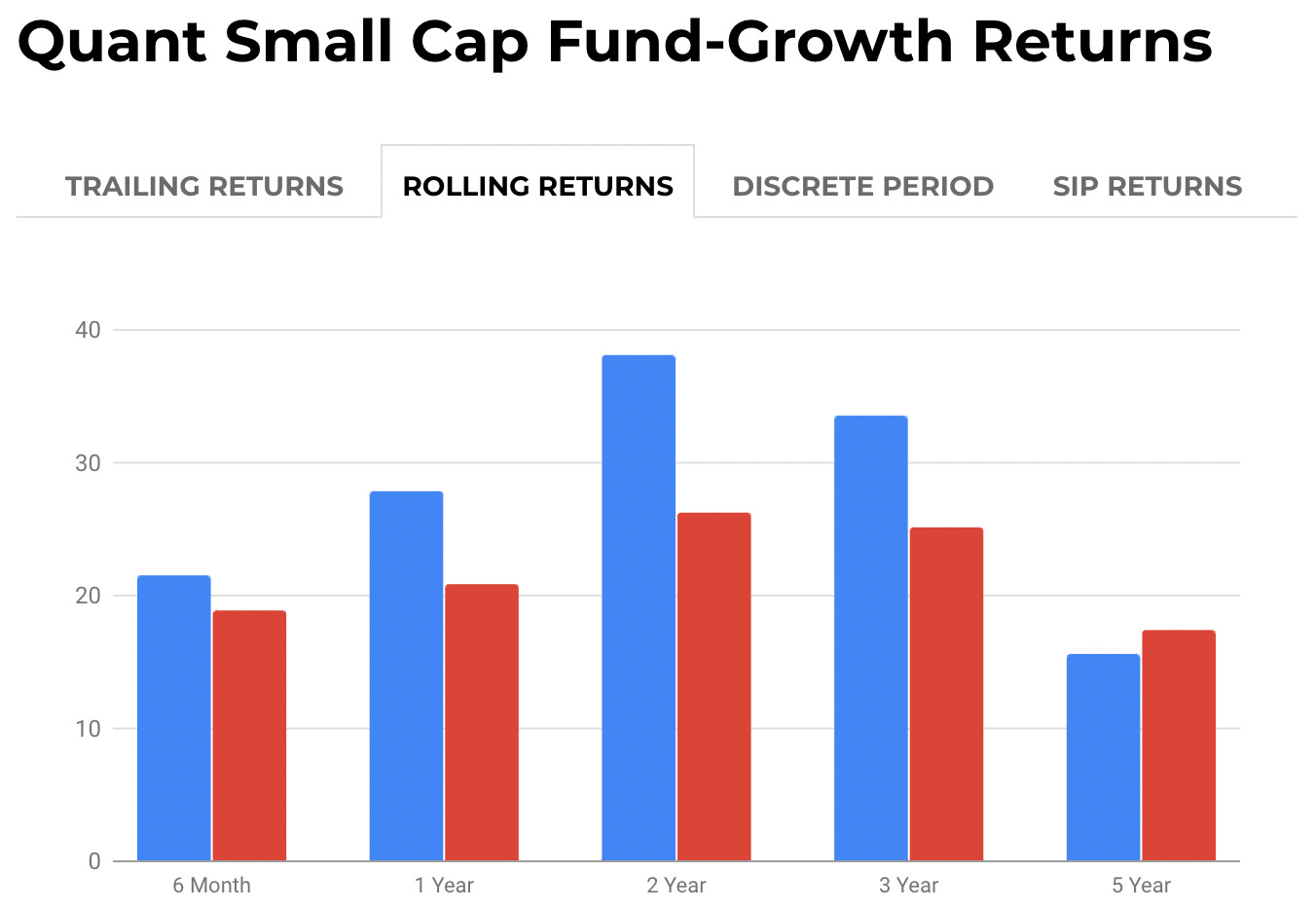

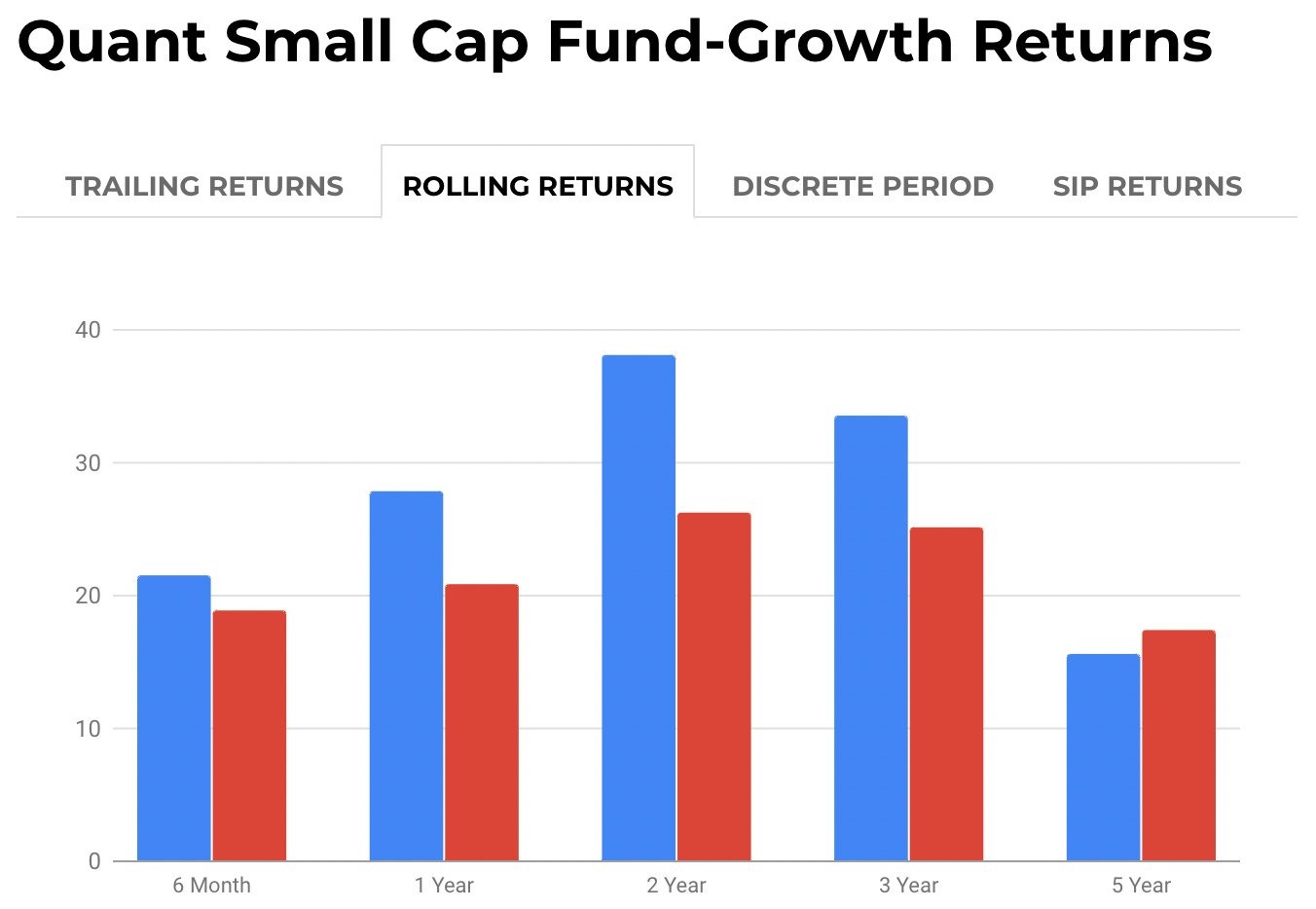

Rolling Returns

We saw what “trailing returns” mean in the context of mutual funds and most people check it before investing in a particular fund but it is the laziest way to choose a mutual fund and I will give you two reasons:

The past 2-3 year returns do not tell much about the mutual fund. It could be that the past three years were a bull market and almost everyone did well. It could also be that the past three years were brutal for the market and most of the funds did bad. If you look at a longer horizon, let’s say 8-10 years, you will be able to see the fund’s performance in all the bull and bear runs, political changes, etc.

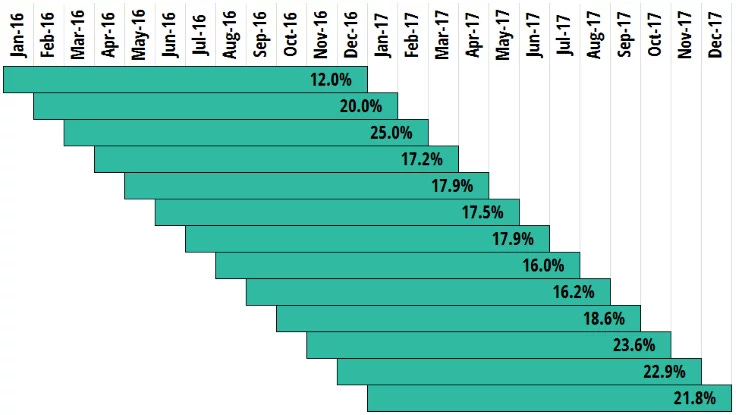

It is the incorrect way to choose a mutual fund. You, as an investor, should look at “Rolling Returns”. Let’s take another example:

Source: Economic Times

The 5-year rolling return for the fund (blue colour) is around 16% and for the category is around 17.5%. So if we start calculating the fund returns from 2014 - 2022, 5-year rolling returns would be the comparison of the return given by any 5-year block as compared to the return given by the category in that 5-year block.

In this case, those 5-year blocks would be 2014-19, 2015-20, 2016-21, 2017-22, and 2018-23. That 16% number we saw above will be the average return of these 5 blocks. In simple words, it is just all the trailing returns put together and calculated continuously like the image below.

You should check for Rolling Returns and not Trailing Returns because the former gives a better idea of the mutual fund’s performance. If the mutual fund is doing well in any block of 5 years in the last 10 years, it is better than a fund that did well in just the last 5 years.

Assets Under Management

This usually matters only for Small Cap Funds because according to a SEBI rule, a mutual fund cannot buy more than 10% of a particular stock.

Let’s say a mutual fund house found an excellent small-cap stock with a market cap of ₹1000 crores and the mutual fund’s AUM is ₹10,000 crores. According to the rule, the mutual fund cannot invest more than ₹100 crores in that particular stock and ₹100 crores is just 1% of the fund’s AUM. Even if the stock goes up by 5 times, it won’t matter much to the fund. Moreover, we have repeatedly seen that when the AUM of a Small Cap fund rises significantly, it stops taking new clients and only allows existing clients to continue SIPs.

High AUM also restricts the amount of return a particular fund can give. Recently, Parag Parekh Flexi Cap Fund hit ₹45,000 crores in AUM and both existing and new investors worried about it. The fund manager clearly stated it’s not a big reason to worry and underscored that whoever wants to invest in the Flexi Cap fund but has concerns about the AUM can invest in the Parag Parekh Tax Saver Fund because it also has the same investment philosophy and is managed by the same team1.

AUM generally doesn’t matter but if you are concerned about it, better look for alternatives.

Fund Manager

Almost all the articles I have read do not describe this factor because almost all the things a funder manager would do to manage risk are captured in the important parameters discussed above. But we are human beings and will build a long relationship with a mutual fund, so why not just get to know the fund manager better (No, I am not asking you to go on a date with the manager)?

The fastest way to learn the investing philosophy of a fund manager is to listen to their interviews. For example, I like Mr Sandeep Tandon (CIO of Quant Mutual Fund) and Mr Rajeev Thakar (CIO of Parag Parekh Mutual Fund). I listen to their interviews and read their articles regularly.

If you deeply understand the philosophy of a mutual fund manager, you will feel more secure and convinced of your investments. It’s like how people who invest in stocks do a deep dive into the stock they are buying, I do the same but not as deep as I would for a stock.

This is my personal opinion. A lot of people do not usually care about the manager but if you are handing over your hard earned savings to someone, you should at least know what that person thinks about investing.

These parameters can be used to choose a mutual fund from a particular category. For example, if you have decided to invest in a Flexi Cap Mutual Fund, you can apply these parameters to choose the best fund among all Flexi Cap funds, and the same goes for Small Cap, Mid Cap, Tax Saver funds, etc.

How many mutual funds to have in your portfolio?

Mutual funds often use storytelling to sell their products, leading investors to make impulsive buying decisions. Investors need to be mindful and focused on their investment goals. Diversification is a valuable quality of mutual funds, but excessive diversification can dilute returns and increase complexity.

Finding the right balance is key. Starting with one fund is a reasonable approach for smaller investments, allowing investors to gradually build their portfolios as their investment grows. Being thoughtful and objective in fund selection helps investors make informed decisions based on their investment goals and risk tolerance. Having a few well-performing funds is more beneficial than having a large number of funds, as it simplifies portfolio management and reduces costs.

Rebalancing the portfolio and maintaining a balanced asset allocation helps manage risks and take advantage of market opportunities. Evaluating fund performance based on long-term market cycles and not reacting to short-term fluctuations is crucial for making informed investment decisions.

Watch this video to learn more about this (not sponsored):

Lump Sum vs SIP, which is better?

Many ask me, “Should we invest in mutual funds or do SIP?”. Let’s answer this question in this part.

After you have decided which mutual fund to invest in and the number of mutual funds to invest in, the next decision is whether we should start SIP or lumpsum investments. But what is SIP? What is Lumpsum?

A Systematic Investment Plan or SIP is a fixed amount you regularly invest in a mutual fund. Let’s say you want to invest ₹10,000 per month in a basket of mutual funds, then you can say “I am doing SIP of ₹10,000” and you can also say “I invest ₹10,000 per month in mutual funds”. A SIP is a type of investment plan which is Systematic - Your mutual fund deducts ₹10,000 every month till you stop it.

Another investment plan that isn’t systematic is Lump sum. In this case, you invest any random amount at any random time. Let’s say you invest ₹50,000 today and then ₹1,00,000 when you receive a bonus from your company after 5 months. These types of investments come under the Lump Sum category.

Which is better - Lump Sum or SIP?

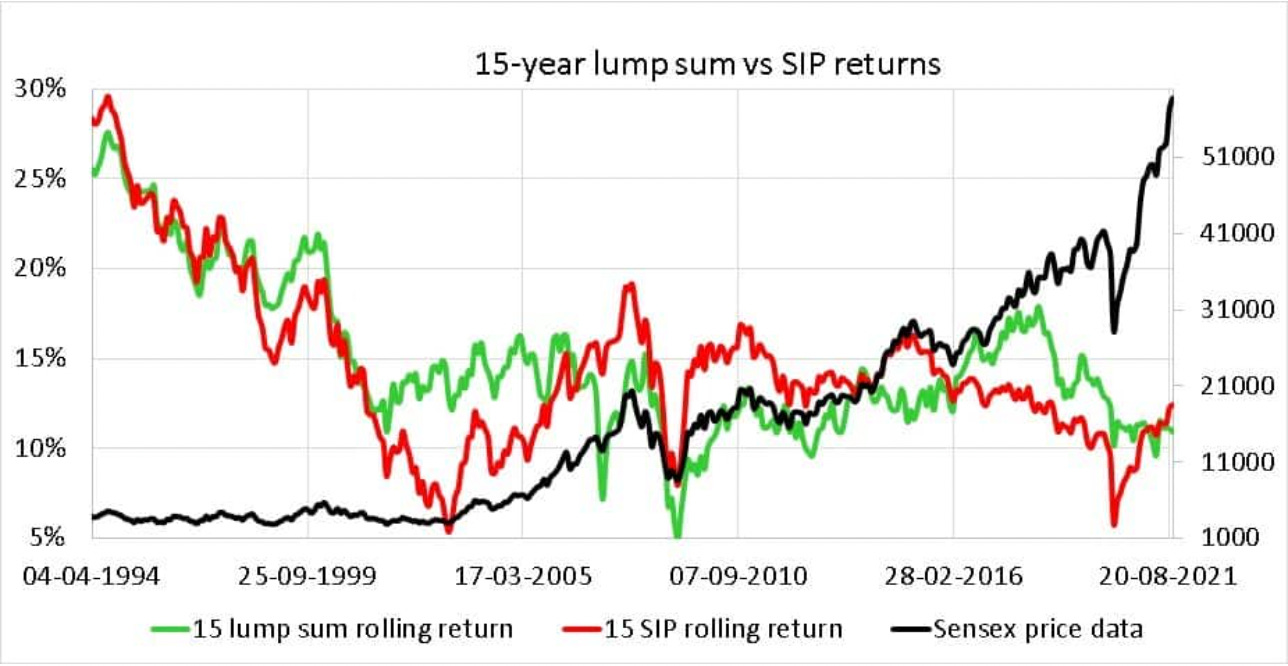

Short answer - It matters a lot when and how you invest. Let’ see this chart:

The chart shows 15-year Lump Sum rolling return vs 15-year SIP returns and you can see that it doesn’t matter whether you go for Lump Sum or SIP, you get almost the same returns. So, if you are planning for a long-term horizon, don’t get into analysis paralysis and start your investing journey.

In my experience, a mix of both works best. If you already have a SIP going on, you can invest excess cash when the market goes down in a lump sum fashion. When the market goes down, the NAV of your mutual fund goes down and when you invest with a low NAV, you can buy more mutual fund units and when the NAV goes up, you get much better returns.

Moreover, psychologically speaking, if you do not have any investments in a mutual fund, you will keep delaying starting a new investment via the Lump sum route. So don’t try to beat your mind because it’s hard, start a SIP and then keep adding lump sum investments when the markets go down.

Another question that I get a lot:

I want to invest ₹10,00,000 in mutual funds. Should I invest it at once or spread it out?

In the long-term, it doesn't matter but it’s hard, as humans, to invest a big amount all at once and see that amount go down by 5% in the next few weeks (assuming that happens). For people like these, there is an option called a Systematic Transfer Plan or STP. In this, you invest all your money, ₹10,00,000 in the case, into a liquid fund of the same mutual fund house, for example, HDFC, and ask them to start STP of a fixed amount, let’s say ₹1,00,000, into the fund which you originally wanted to invest, let’s say HDFC Flexi Cap fund. Each month, ₹1,00,000 will be deducted from that liquid fund and be invested in the Flexi Cap Fund and the process stops after 10 months.

What is the best date for starting your SIP journey?

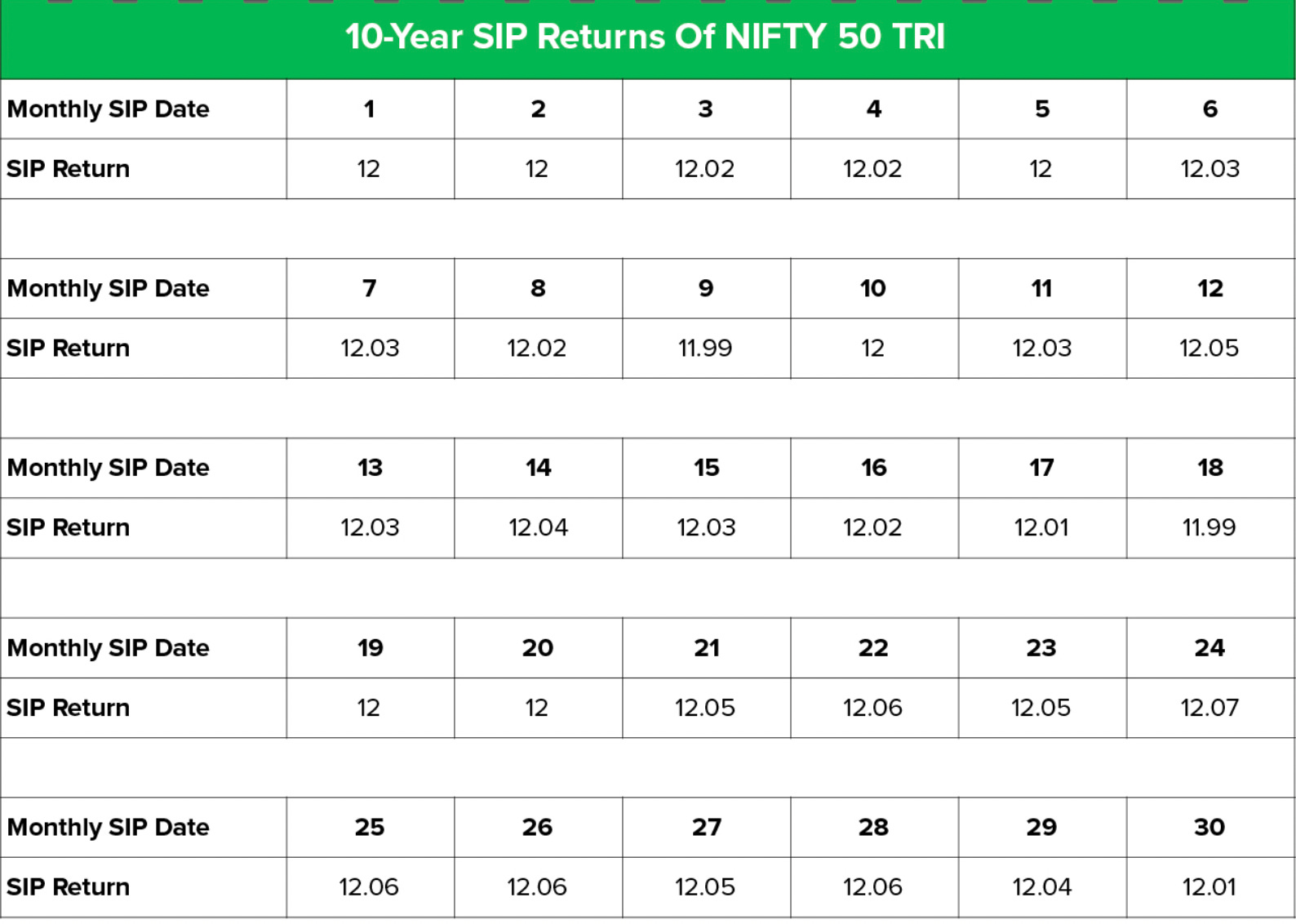

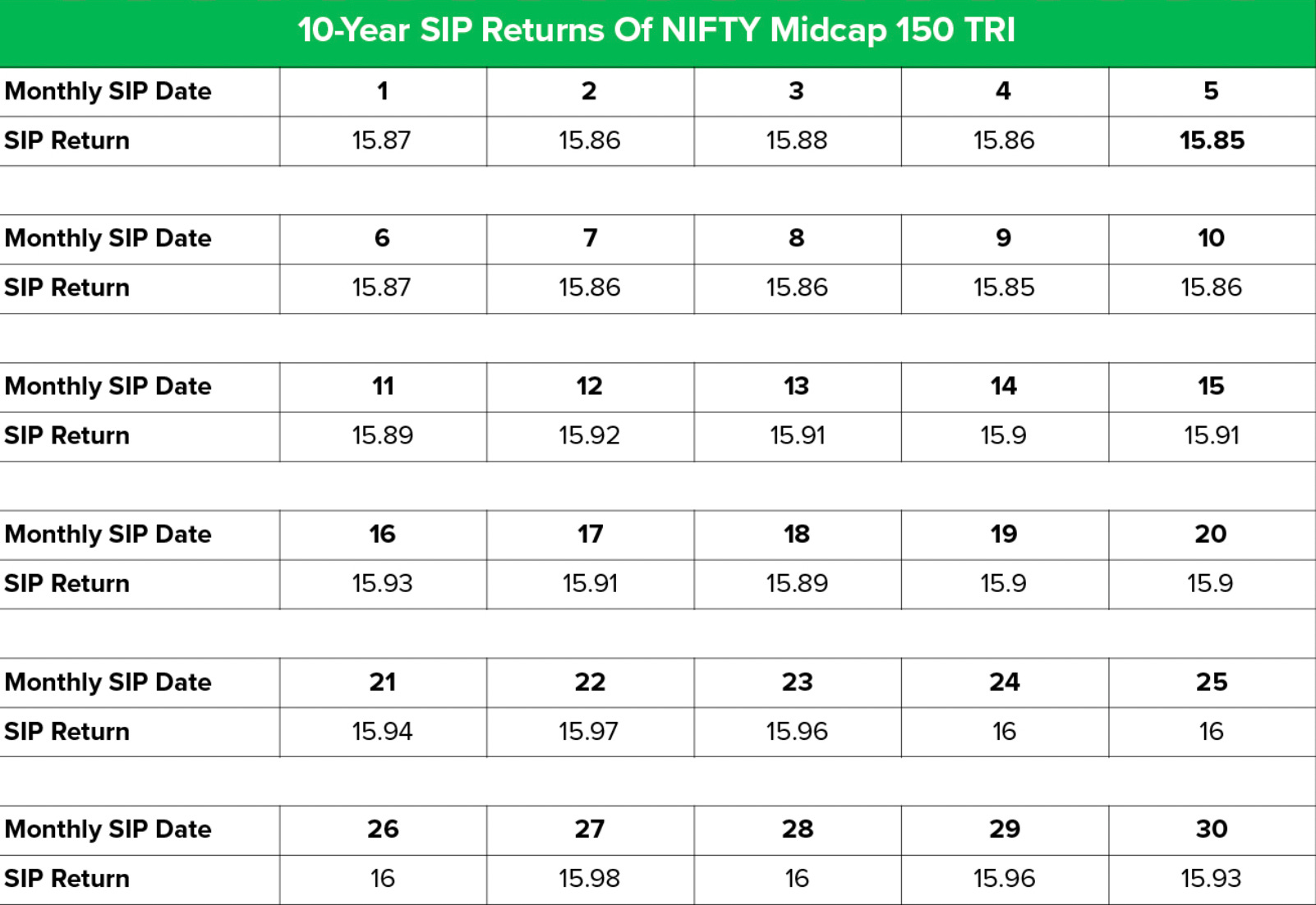

Now you have decided everything and when you are filling out the form to start your SIP in any mutual fund, one question they will ask “Which date of the month should we deduct this amount?”, and there are many options. How should you decide which date will give you the best returns?

Answer: It doesn’t matter and I will prove that using data.

This image is for Nifty 50 returns

This image is for the Nifty Mid Cap 150 Index:

This image is for the Nifty Small Cap 250 Index:

So you can see there is almost no difference. Don’t get into analysis-paralysis and just start your mutual fund investing journey today.

Three things to keep in mind after you have chosen your mutual fund:

If you are investing for long-term, avoid ETFs, read this to know why.

You should always invest in a “Direct” fund and not a “Regular” fund, read this article to find out why.

To create massive long-term wealth, avoid huge churn, i.e. stay invested for as long as you can, it will surely help you. DO NOT TRY TO TIME THE MARKET!!

Stay focused, and do not get swayed by stock tips because it is harder to create huge long-term wealth using stocks, read this to know why.

DISCLAIMER: Mutual Funds are subject to market risk. Do your research before investing your hard-earned money. Please read all the scheme documents carefully before investing.

This is the first draft that I created and completed on 31st March 2024 but is just a start. As I learn more and more things, I will keep updating it and probably after 4-6 months, this will become the ultimate guide. So save it and share it with everyone you know.

https://amc.ppfas.com/knowledge-center/notes-by-rajeev-thakkar/2023/a-few-thoughts-on-the-parag-parikh-flexicap-fund-completing-10-years-since-launch.pdf

Just wow... one stop place to know the basics simplified and well explained.. Thankyou som much for this article..